2023 audit cites Dublin City Schools for ‘lack of financial controls’

Auditors note pattern of overspending that only got worse in subsequent years.

The Dublin City Schools finished fiscal year 2023 with a $3.3 million surplus, but was already set on the course of overspending and “lack of financial controls” that eventually landed the district in crisis, according to the long-awaited FY23 audit.

The positive fund balance came only after the district spent $2.2 million above that year’s revenue, which included more than $6 million in federal COVID funds. The report only covered FY23, but auditors also reviewed subsequent fiscal year documents that showed the district’s overspending only got worse.

The schools appear to have overspent by $5.2 million in fiscal year 2024 and $3.8 million in 2025, according to the report, meaning the system started the current fiscal year $5.7 million in the hole.

“The lack of budgetary and spending controls has led to a significant deterioration of the school district’s financial condition,” auditors from the firm Mauldin & Jenkins wrote in their report.

The audit also shows another concerning trend surface as the district delayed making some payments to the State Health Benefit Plan, postponing May and June’s payments until January 2024.

That practice first brought the system’s cashflow predicament under public scrutiny last August, when the Georgia Department of Community Health alerted state education officials that Dublin City did not pay the health plan for the entirety of FY 2025 and also owed more that $5 million in past-due payments. Officials found the district also owed $780,512 withheld from employees’ pay but not sent to the Department of Community Health.

The state Department of Education later found other “operational deficiencies,” which included the system not having completed an audit since 2021, and projected the district would finish the current year with a $13.4 million deficit. School officials have said the deficit should be closer to $5 million after spending cuts that included eliminating about 50 jobs.

Local lawmakers later requested a special audit that confirmed the root causes of the crisis – overhiring and overpaying employees, wasteful spending and lax oversight – while also identifying specific concerns ranging from late tax payments to the IRS, “abnormally” high credit card spending and unwarranted travel and expenditures. The special audit also pointed to instances of family members traveling on out-of-town leadership retreats at the system’s expense and undocumented payments to a local florist.

That led Dublin Circuit District Attorney Harold McLendon to formally request the Georgia Bureau of Investigation conduct a criminal investigation in the district’s finances. A GBI spokesperson confirmed last week that an investigation is ongoing.

The report also laid the blame for the audit’s tardiness on the district, with auditors encountering “numerous delays in the receipt of information from management.”

“We did not receive final documents we needed until November 2025,” Mauldin & Jenkins accountant Hope Pendergrass explained to Dublin City Board of Education members last week.

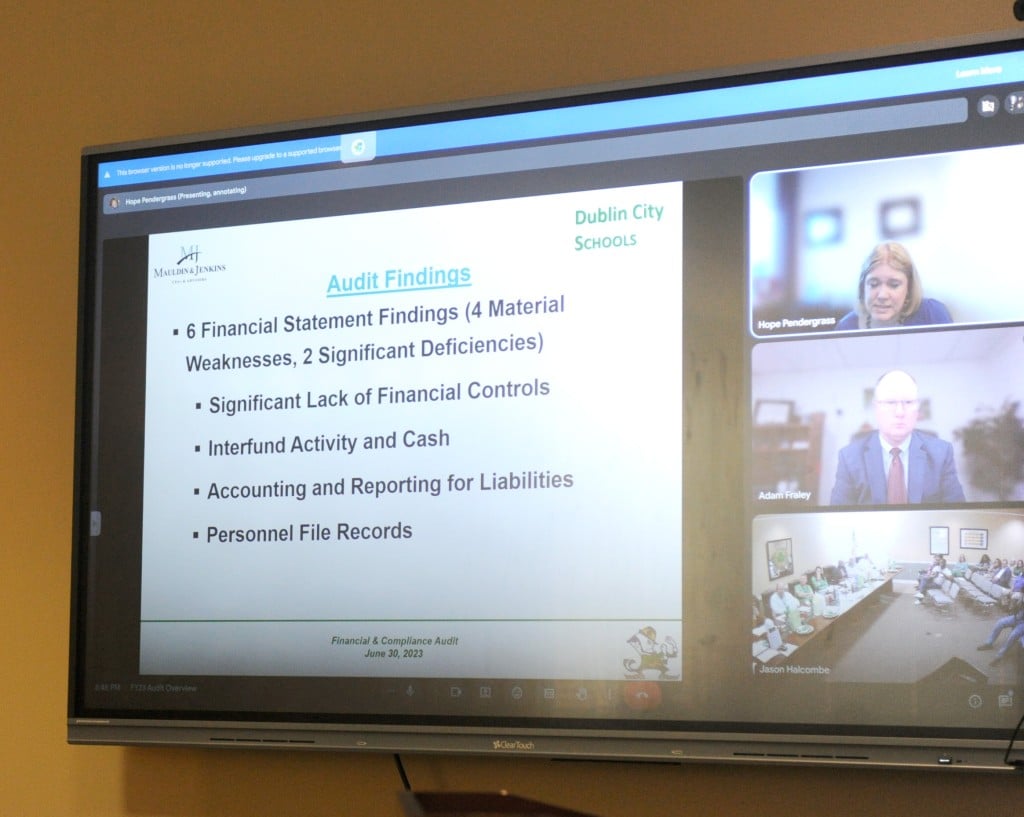

The audit included more than a half-dozen findings labeled as “material weaknesses” and “significant deficiencies.” It also included a citation labeled “Title I – Maintenance of Effort” that, should it happen again in any of the next five years, could jeopardize federal funding in the future.

School systems are required by law to spend – on either an aggregate or per capita basis – an amount of local funds, or combination of local and state funds, equal to the amount spent the prior year.

“The school district did not meet maintenance of effort for the fiscal year. … Should the district fail to meet (maintenance of effort) requirements in the subsequent five years, (Georgia Department of Education) may be required to reduce federal funding.”

Other items cited in the audit as material weaknesses or significant deficiencies were:

• Significant Lack of Financial Controls

The audit says the school district “displayed a significant lack of budgetary oversight and expenditure control.” The system also did not complete its year-end closing procedures and provide items for the audit in a timely manner, and key reconciliations – including bank statements, tax reconciliations, accounts payable and preparation of the schedule of expenditures of federal awards.

The delay in closing the books and completing the audit has “several potential adverse effects” including loss of fiscal oversight. Outdated information “diminishes its usefulness to the governing board in making current-year adjustments.”

• Interfund Activity and Cash

Interfund receivables and payables, when transactions occur between individual funds for goods or services rendered, were not properly stated for the period. Transfers when funds were not expected to be repaid were not recorded. Auditors recommended the district strengthen internal controls over interfund activity to ensure transfers are properly stated at year’s end.

• Accounting and Reporting of Expenses and Liabilities

Auditors cited the delay in insurance payments to the State Health Benefit Plan when noting the district’s lack of “timely reporting” of liabilities. They encouraged the district to “reconcile all liability balances in a timely manner to ensure all transactions are being properly recognized during the correct period.”

• Personnel File Records

Changes were not documented and included in the appropriate personnel files. “We were unable to verify that any changes noted State Health Benefit Plan transmission files were valid changes to various employees’ personnel files for the year,” auditors said.

• Management of property tax receivables, revenue and unavailable revenue

Auditors noted that several adjustments had to be made in those three areas and recommended the district update its monthly reconciliation process for property taxes.

•Improper Recording of Debt Service Payments

Debt service payments were not recorded correctly, requiring an adjustment to properly state amounts. Auditors recommended the district update is year-end closing process to include formal reconciliation of long-term debts.

• Education Stabilization Fund – Equipment and Real Property Management

The district did not maintain property records or required physical inventory of property or equipment purchased with federal funding.

• Title 1 – Grants to Local Educational Agencies – Annual Report Card, High School Graduation Rate

Auditors recommended the district monitor codes used and obtain appropriate documentation for removing a student from a cohort, the group of students who enter a grade level the same year and are expected to graduate at the same time. Auditors tested for appropriate documentation for a student who was removed from the adjusted cohort, but the district failed to provide the documentation. Additionally, the district later realized the incorrect code was used to remove the student.

School board member James Lanier asked at last week’s meeting if Mauldin & Jenkins had noticed any of the same problems in 2022’s audit – which was only recently completed and showed the district ending that fiscal year with fund balance of more than $5 million.

“Not like this,” Pendergrass said.

Board Chairwoman Amanda Smith said that interim Superintendent Marcee Pool and staff have worked to implement more financial safeguards in recent months.

“The audit talks about no financial controls. Well, there are controls now,” Smith said.

Author

Related Articles

Remembering AJ: Pre-schoolers raise money to honor Stuckeys

Children and teachers donned their favorite superhero capes, masks and outfits as they donated money to a local organization in honor of a former student.

City council plans to look into ordinances to help with nuisance issues

Dublin mayor and city council members promised to examine ordinances to tackle nuisance situations pestering residents.

Retired teacher, former student honored to win St. Patrick’s Awards

The St. Patrick’s Senior Adult of the Year and Man of the Year have something in common. She taught him in school.

James Deal was shocked when his name was called for the Man of the Year, but he was glad to hear his former teacher Jeanette Fulford’s name called for the Senior Citizen of the Year award moments later.